The latest report from business intelligence provider Visiongain offers comprehensive analysis of the global next-generation energy storage technologies market. Visiongain estimates that this market will reach a capacity of 1,674 MW IN 2018.

Now: “Evaluating Energy Storage for Summer Grid Resiliency”. This is an example of a headline coming out of Eos Energy storage that you need to know about as this company looks to expand its next-generation grid scale energy storage technology – but more importantly, you need to read Visiongain’s objective analysis of how this will impact your company and the industry more broadly. How are you and your company reacting to this news? Are you sufficiently informed?

How this report will benefit you

This report contains objective market forecasts using a number of inputs and market research as well as general overviews of the technologies that are up and coming in the storage sector.

In this brand-new report, you find over 250 in-Depth tables and figures as well as three exclusive interviews with market leading companies Younicos, Eos Energy Storage and EGP North America.

The 242-page report provides clear, detailed insight into the global next-generation energy storage market. Discover the key drivers and challenges affecting the market.

By ordering and reading our brand-new report today you stay better informed and ready to act.

Report Scope

• Global Next-Generation Energy Storage Capacity (MW) And Value ($m) Forecasts From 2018-2028

• Next Generation Energy Storage Technologies (EST) Capacity Forecasts (MW) From 2018-2028

• Mechanical Technologies Forecast 2018-2028

• Chemical Technologies Forecast 2018-2028

• Electrical Technologies Forecast 2018-2028

• Electrochemical Technologies Forecast 2018-2028

• Thermal Technologies Forecast 2018-2028

• Regional Next-Generation Energy Storage Capacity (MW) And Value ($m) Forecasts From 2018-2028 Covering

• Europe Forecast 2018-2028

• North-America Forecast 2018-2028

• China and Japan Forecast 2018-2028

• Rest of the World Forecast 2018-2028

• Profile Of 10 Leading Companies In The Next-Generation Energy Storage Sector

• Johnson Controls

• LG Chem Ltd.

• Duke Energy Corporation

• NextEra Energy Inc.

• Edison International

• Samsung SDI Co. Ltd.

• Mitsubishi Electric Corporation

• BYD Co. Ltd.

• Robert Bosch GmbH

• ABB Group

• 3 interviews with key opinion leaders

• Philippe Bouchard – Eos Energy Storage

• Philip Hiersemenzel – Younicos

• Krista Barnaby – EGP North America

How will you benefit from this report?

• Keep your knowledge base up to speed. Don’t get left behind

• Reinforce your strategic decision-making with definitive and reliable market data

• Learn how to exploit new technological trends

• Realise your company’s full potential within the market

• Understand the competitive landscape and identify potential new business opportunities & partnerships

Who should read this report?

• Anyone within the energy storage or transmission and distribution markets.

• Renewable energy companies

• Utilities

• Battery manufacturers

• R&D staff

• Technologists

• Research scientists

• Business development managers

• Marketing managers

• Market analysts

• Consultants

• Suppliers

• Investors

• Banks

• Government agencies

• Industry associations

• Contractors

Visiongain’s study is intended for anyone requiring commercial analyses for the energy storage market and leading companies. You find data, trends and predictions.

Buy our report today Next Generation Energy Storage Technologies (EST) Market Forecast 2018-2028: Analysis of Technology Maturity, Performance & Commercialisation of Mechanical (Innovative Pumped Hydro Storage (PHS), Advanced Adiabatic Compressed Air Energy Storage (AA-CAES), Isothermal CAES & Liquid Air Energy Storage (LAES)), Chemical (Hydrogen Storage & Fuel Cells), Electrical (Superconducting Magnetic Energy Storage (SMES)), Electrochemical (Lithium-Air, Lithium-Sulphur, Magnesium-Ion & Zinc-Air Batteries) & Thermal Technologies for Renewable Energy Sources (RES) Integration. Avoid missing out by staying informed – get our report now.

Visiongain is a trading partner with the US Federal Government

CCR Ref number: KD4R6

1. Report Overview

1.1 Global Energy Storage Technology Market Overview

1.2 Why You Should Read This Report?

1.3 Benefits of This Report

1.4 Structure of this Report

1.5 Key Questions Answered by This Analytical Report

1.6 Who is this Report for?

1.7 Market Definition

1.8 Methodology

1.9 Frequently Asked Questions (FAQ)

1.10 Associated Visiongain Reports

1.11 About Visiongain

2. Introduction to the Energy Storage Technologies Market

2.1 An Introduction To Established And Emerging Energy Storage Technologies

2.2 Installed Energy Storage Capacity

2.3 The Rise Of Emerging Energy Storage Technologies

2.4 The Key Applications Of Established And Emerging Energy Storage Technologies

3. The Drivers And Restraints Of Next-Generation Energy Storage Technologies

3.1 An Introduction To The Dynamics Of The Market

3.2 The Factors That Will Drive And Restrain The Market

3.2.1 Rising Energy Prices Indirectly Incentivise EST

3.2.2 Investments In EST Research, Development And Demonstration

3.2.3 The Importance Of Renewable Energy Integration

3.2.4 Smart Grids And Distributed Power Generation Systems

3.2.5 Growing Electricity Demand

3.2.6 The Developing Electric Vehicle Market As A Growth Factor

3.2.7 The High Capital Costs Of Emerging Energy Storage Technologies

3.2.8 Limited Cost Recovery Opportunities

3.2.9 The Policy And Regulatory Challenges Ahead

3.2.10 The Impact Of Weak Market Demand For ESTs

3.2.11 Geographical And Spatial Constraints On EST

3.2.12 The Need For Large-Scale Demonstration Projects

3.2.13 Raw Material Availability

3.2.14 Technology Development And Deployment Patterns

3.2.15 The Limitations Of Established Energy Storage Technologies

3.2.16 Long Investment Cycles

3.2.17 Opportunities For Home Energy Storage Arbitrage

3.2.18 Global Next Generation Energy Storage Technologies Market Forecast By Technologies 2018-2028

4. Next Generation Mechanical Energy Storage Technologies 2018-2028

4.1.1 An Introduction To Innovative Pumped Hydro Storage

4.1.2 The Nature Of The Innovation

4.1.3 The Performance Characteristics Of Innovative PHS Installations

4.1.4 Applications And Key Competitors Of Innovative PHS

4.1.5 Current Deployment Of Innovative PHS

4.1.6 Drivers And Restraints Of Innovative PHS

4.1.7 The Outlook For Innovative PHS

4.1.8 Companies And Stakeholders Involved In The Innovative PHS Market

4.2 Adiabatic And Isothermal Compressed Air Energy Storage

4.2.1 An Introduction To Adiabatic And Isothermal Compressed Air Energy Storage

4.2.2 The Nature Of The Innovation

4.2.3 The Performance Characteristics Of Adiabatic And Isothermal CAES

4.2.4 The Applications And Key Competitors Of Advanced CAES

4.2.5 Current Deployment Of Compressed Air Energy Storage

4.2.6 Drivers And Restraints Of Advanced Compressed Air Energy Storage

4.2.7 The Outlook For Advanced CAES

4.2.8 Companies And Stakeholders Involved In The Advanced CAES Market

4.3 Liquid Air Energy Storage (LAES)

4.3.1 An Introduction To LAES

4.3.2 The Nature Of The Innovation

4.3.3 The Performance Characteristics Of LAES

4.3.4 The Applications And Key Competitors Of LAES

4.3.5 Current Deployment Of LAES

4.3.6 Drivers And Restraints Of The LAES Market

4.3.7 The Outlook For LAES

4.3.8 Companies And Stakeholders Involved In The LAES Market

5. Next Generation Chemical Energy Storage Technologies 2018-2028

5.1 Large-Scale Hydrogen Energy Storage Systems And Hydrogen Fuel Cells

5.1.1 An Introduction To Large-Scale Hydrogen Energy Storage Systems And Hydrogen Fuel Cells

5.1.2 The Nature Of Innovation

5.1.3 The Performance Characteristics Of Large-Scale Hydrogen Energy Storage Systems And Hydrogen Fuel Cells

5.1.4 The Applications And Key Competitors Of Large-Scale Hydrogen Storage Systems And Hydrogen Fuel Cells

5.1.5 Current Deployment Of Large-Scale Hydrogen Energy Storage Systems And Hydrogen Fuel Cell

5.1.6 Drivers And Restraints Of Large-Scale Hydrogen Storage Systems And Hydrogen Fuel Cells

5.1.7 The Outlook For Large-Scale Hydrogen Energy Storage Systems And Hydrogen Fuel Cells

5.1.8 Companies And Stakeholders Involved In The Hydrogen And Fuel Cells Energy Storage Market

6. Next-Generation Electrical Energy Storage Technologies Analysis

6.1 Superconducting Magnetic Energy Storage (SMES)

6.1.1 An Introduction To SMES

6.1.2 The Nature Of Innovation

6.1.3 The Performance Characteristics Of SMES

6.1.4 The Applications And Key Characteristics And Key Competitors Of SMES

6.1.5 Current Deployment Of SMES

6.1.6 Drivers And Restraints Of SMES

6.1.7 The Outlook For SMES

6.1.8 Companies And Stakeholders Involved In The SMES Market

7. Next-Generation Electrochemical Energy Storage Technologies 2018-2028

7.1 An Introduction To Next-Generation Battery Technologies

7.2 The Key Drivers Of Innovation In The Market

7.3 Key Patterns Of Innovation In The Market

7.4 Lithium-Air

7.4.1 Nature Of The Innovation

7.4.2 The Performance Characteristics Of Lithium-Air Batteries

7.4.3 The Applications And Key Competitors Of Lithium-Air Batteries

7.4.4 Current Deployment Of Lithium-Air Batteries

7.4.5 The Drivers And Restraints Of The Lithium-Air Batteries Market

7.4.6 The Outlook For Lithium-Air Batteries

7.4.7 Key Companies And Stakeholders Involved In The Lithium-Air Battery Market

7.5 Lithium-Sulphur (Li-S)

7.5.1 Nature Of The Innovation

7.5.2 The Performance Characteristics Of Lithium-Sulphur Batteries

7.5.3 The Applications And Key Competitors Of Lithium-Sulphur Batteries

7.5.4 Current Deployment Of Lithium-Sulphur Batteries

7.5.5 The Drivers And Restraints Of The Lithium-Sulphur Battery Market

7.5.6 The Outlook For Lithium-Sulphur Batteries

7.5.7 Key Companies And Stakeholders Involved In The Lithium-Sulphur Battery Market

7.6 Magnesium-Ion (Mg-Ion)

7.6.1 Nature Of The Innovation

7.6.2 The Performance Characteristics Of Magnesium-Ion Batteries

7.6.3 The Applications And Key Competitors Of Magnesium-Ion Batteries

7.6.4 Current Deployment Of Magnesium-Ion Batteries

7.6.5 The Drivers And Restraints Of Magnesium-Ion Batteries

7.6.6 The Outlook For Magnesium-Ion Batteries

7.6.7 Key Companies And Stakeholders Involved In The Magnesium Ion Battery Market

7.7 Zinc-Air (Zn-Air)

7.7.1 Nature Of The Innovation

7.7.2 The Performance Characteristics Of Zinc-Air Batteries

7.7.3 The Main Applications And Key Competitors Of Zinc-Air Batteries

7.7.4 Current Deployment Of Zinc-Air Batteries

7.7.5 The Drivers And Restraints Of The Zinc Air Battery Market

7.7.6 The Outlook For Zinc-Air Batteries

7.7.7 Key Companies And Stakeholders In The Zinc-Air Battery Market

7.8 Concluding Remarks On Emerging Battery Storage Technologies

8. Next-Generation Thermal Energy Storage Technologies 2018-2028

8.1 An Introduction to Next-Generation Thermal Battery Storage Technologies

9. Expert Opinion

9.1 Philippe Bouchard – Eos Energy Storage

9.1.1 About Eos

9.1.1.1 Composition of Znyth Battery

9.1.2 Future Plans for Eos

9.1.3 Genesis Project

9.1.4 The Future of the Industry

9.2 Philip Hiersemenzel – Younicos

9.2.1 Overview

9.2.1.1 Residential or industrial Use?

9.2.2 Market Outlook

9.3 Krista Barnaby – EGP North America

9.3.1 Background

9.3.2 key Markets

9.3.3 Characteristics of EGP’s Technologies

9.3.4 Future for the Industry

10. PESTEL Analysis

11. Established and Emerging Energy Storage Technologies, a Comparative Analysis

12. The Global Landscape of the Emerging Energy Storage Technologies Market 2018-2028

13. The Leading Companies in the Next Generation Energy Storage Technologies Market

13.1 Johnson Controls

13.1.1 Johnson Controls Total Company Sales 2011-2017

13.1.2 Johnson Controls Sales in the Energy Storage Technologies Market 2011-2017

13.2 LG Chem Ltd.

13.2.1 LG Chem Ltd. Total Company Revenue 2012-2016

13.3 Duke Energy Corporation

13.3.1 Duke Energy Corporation Total Company Sales 2011-2017

13.3.2 Duke Energy Corporation Total Company Revenues in the Energy Storage Technologies Market 2014-2017

13.4 NextEra Energy Inc.

13.4.1 NextEra Energy, Inc. Total Company Sales 2011-2017

13.4.2 NextEra Energy, Inc. Sales in the Renewable Technologies Market 2012-2017

13.5 Edison International

13.5.1 Edison International Total Company Sales 2011-2017

13.6 Samsung SDI Co. Ltd.

13.6.1 Samsung SDI Co. Ltd. Total Company Sales 2011-2017

13.6.2 Samsung SDI Co. Ltd. Revenue from LI-Ion Batteries 2015-2017

13.7 Mitsubishi Electric Corporation

13.7.1 Mitsubishi Electric Corporation Total Company Sales 2011-2017

13.7.2 Mitsubishi Electric Corporation Revenue from Energy and Electric Systems 2011-2017

13.8 BYD Co. Ltd.

13.8.1 BYD Co. Ltd. Total Company Sales 2011-2017

13.8.2 BYD Co. Ltd. Revenue from Rechargeable Battery and Photovoltaic 2011-2017

13.9 Robert Bosch GmbH

13.9.1 Robert Bosch GmbH Total Company Sales 2013-2017

13.9.2 Robert Bosch GmbH Revenue from Energy and Building technology 2015-2017

13.10 ABB group

13.10.1 ABB Group Total Company Sales 2011-2017

13.10.2 ABB Group Revenues in the Electrification Products Market 2015-2017

13.11 Other Companies Involved in the Next Generation Energy Storage Technologies Market 2016

14. Conclusions and Recommendations

14.1 Drivers and Restraints of the Next-Generation Energy Storage Technologies Market

14.2 The Outlook for Innovative Pumped Hydro Storage

14.3 The Outlook for Advanced Compressed-Air Energy Storage

14.4 The Outlook for Liquid-Air Energy Storage

14.5 The Outlook for Large-Scale Hydrogen Storage Systems and Hydrogen Fuel Cells

14.6 The Outlook for Superconducting Magnetic Energy Storage

14.7 The Outlook for Next-Generation Batteries

15. Glossary

List of Tables

Table 1.1 Example of Standardised Metric Used for the Comparison of Energy Storage Technologies in Radial Graphs Presented Throughout This Report

Table 2.1 Global Next Generation Energy Storage Technologies Market Forecast 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 2.2 List and Description of Main EST Applications

Table 3.1 Recent Demonstration Projects Funded by ARRA (Name, EST, MW Size, $m Cost, Planned Application)

Table 3.2 Global EST Market Drivers & Restraints

Table 3.3 Global Next Generation Energy Storage Technologies Market Forecast By Technology 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 4.1 Global Next Generation Energy Storage Technologies Market Forecast, By Mechanical Energy Storage Technology 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 4.2 PHS main characteristics (Lifetime, Capacity MW, Efficiency %, Maturity)

Table 4.3 List of all Operating Innovative Pumped Hydro Installations (Name, Location, Capacity MW, Type, Commissioning)

Table 4.4 Pumped Hydro Storage (PHS) Market Drivers & Restraints

Table 4.5 List of all Planned Innovative Pumped Hydro Installations (Name, Location, Capacity MW, Type, Commissioning)

Table 4.6 Performance Characteristics of Conventional and Advanced CAES (Lifetime, Capacity MW, Efficiency %, Maturity)

Table 4.7 Installed CAES Capacity by National Market (MW)

Table 4.8 Key Diabatic and Adiabatic Compressed Air Energy Projects (Name, Location, Capacity MW, Type, Commissioning)

Table 4.9 Advanced CAES Market Drivers & Restraints

Table 4.10 Project Details for the Poleggio-Loderio Pilot AA-CAES Plant (Name, Location, Companies and Organisations Involved, Capacity kW, Type, Commissioning Date)

Table 4.11 The Main Characteristics of Liquid Air Energy Storage (Lifetime, Capacity MW, Efficiency %, Maturity)

Table 4.12 Drivers and Restraints of the LAES technology

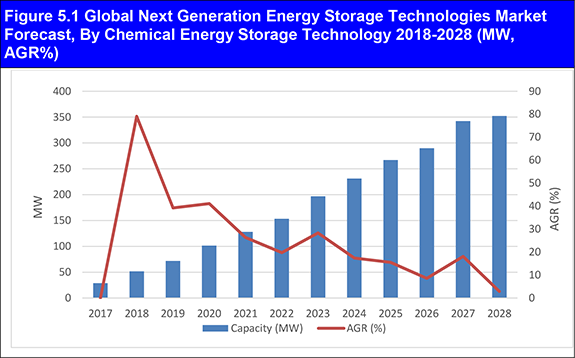

Table 5.1 Global Next Generation Energy Storage Technologies Market Forecast, By Chemical Energy Storage Technology 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 5.2 Hydrogen Main Characteristics (Lifetime, Capacity, Efficiency, Maturity)

Table 5.3 Large Scale Hydrogen Energy Storage and Hydrogen Fuel Cell Drivers & Restraints

Table 6.1 Performance characteristics SMES (Lifetime, Capacity MW, Efficiency %, Maturity)

Table 6.2 Drivers & Restraints of the SMES Market

Table 7.1 Global Next Generation Energy Storage Technologies Market Forecast, By Electrochemical Energy Storage Technology 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 7.2 Main Performance Characteristics of Lithium-Air Batteries (Energy density, Cycle life, Efficiency, Maturity)

Table 7.3 Lithium-Air Batteries Market Drivers & Restraints

Table 7.4 Main Performance Characteristics of Lithium-sulphur Batteries (Energy Density, Cycle Life, Efficiency, Maturity)

Table 7.5 Lithium-sulphur Batteries Market Drivers and Restraints

Table 7.6 Main Performance Characteristics for Magnesium Ion Batteries (Energy Density, Cycle Life, Efficiency, Maturity)

Table 7.7 Magnesium Ion Batteries Market Drivers & Restraints

Table 7.8 Main Performance Characteristics of Zinc Air Batteries (Energy Density, Cycle Life, Efficiency, Maturity)

Table 7.9 Zinc Air Batteries Market Drivers & Restraints

Table 8.1 Global Next Generation Energy Storage Technologies Market Forecast, By Thermal Energy Storage Technology 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 10.1 PESTEL Analysis of the Emerging EST Market

Table 11.1 Comparison of Key Established and Emerging Energy Storage Technologies (Maturity, Capacity, Efficiency, Lifecycle)

Table 11.2 The Development Stage and Challenges of Established and Emerging Energy Storage Technologies

Table 12.1 Global Next Generation Energy Storage Technologies Market Forecast, By Region 2018-2028 ($bn, AGR %, CAGR %, Cumulative)

Table 12.2 Innovative PHS Submarket Forecast 2018-2028 ($m, AGR %, CAGR %, Cumulative)

Table 12.3 North America Next Generation Energy Storage Technologies Market Forecast 2018-2028 ($bn, AGR %, CAGR %, Cumulative)

Table 12.4 North America Next-Generation EST Market Drivers & Restraints

Table 12.5 Recent Projects to Receive Funding from European Commission

Table 12.6 European Next-Generation EST Market Drivers & Restraints

Table 12.7 China & Japan Next Generation Energy Storage Technologies Market Forecast 2018-2028 ($bn, AGR %, CAGR %, Cumulative)

Table 12.8 Asian Next-Generation EST Market Drivers & Restraints

Table 13.1 Johnson Controls 2018 (CEO, Total Company Sales US$m, Sales Related to EST US$m, Share of Sales Related to EST %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website

Table 13.2 Johnson Controls Total Company Sales 2011-2017 (US$m, AGR %)

Table 13.3 Johnson Controls Sales in the Energy Storage Technologies Market 2011-2017 (US$m, AGR %)

Table 13.4 LG Chem Ltd. 2018 (CEO, Total Company Revenue US$m, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.5 LG Chem Ltd. Total Company Revenue 2011-2016 (US$m, AGR %)

Table 13.6 LG Chem Ltd. Sales in the Energy Storage Technologies Market 2011-2015 (US$m, AGR %)

Table 13.7 Duke Energy Corporation Profile 2017 (CEO, Total Company Revenue US$m, Revenue from the storage Market US$m, Share of Company Sales from Energy Storage Technologies Market %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.8 Duke Energy Corporation Total Company Revenue 2011-2017 (US$m, AGR %)

Table 13.9 Table 13.9 Duke Energy Corporation Revenue in the Energy Storage Technologies Market 2014-2017 (US$m, AGR %)

Table 13.10 NextEra Energy, Inc. Profile 2018 (CEO, Total Operating Revenue US$m, Sales in the Renewable Energy Market US$m, Share of Company Sales from Renewable Energy %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.11 NextEra Energy, Inc. Operating Revenue 2011-2017 (US$m, AGR %)

Table 13.12 NextEra Energy, Inc. Sales in the Renewable Technologies Market 2010-2016 (US$m, AGR %)

Table 13.13 Edison International 2018 (CEO, Total Company Revenue US$m, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.14 Edison International Total Company Sales 2011-2017 (US$m, AGR %)

Table 13.15 Samsung SDI Co. Ltd. 2018 (CEO, Total Company Revenue US$m, Revenue from Li-Ion Battery US$m, Share of Company Sales from Li-Ion %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.16 Samsung SDI Co. Ltd. Total Company Revenue 2011-2017 (US$m, AGR %)

Table 13.17 Samsung SDI Co. Ltd. Revenue from LI-Ion Market 2015-2017 (US$m, AGR %)

Table 13.18 Mitsubishi Electric Corporation Profile 2018 (CEO, Total Company Revenue US$m, Revenue from Energy and Electric Systems US$m, Share of Company Sales from Energy and Electric Systems %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.19 Mitsubishi Electric Corporation Total Company Sales 2011-2017 (US$m, AGR %)

Table 13.20 Mitsubishi Electric Corporation Revenue from Energy and Electric Systems 2011-2017 (US$m, AGR %)

Table 13.21 BYD Co. Ltd Profile 2016 (CEO, Total Company Revenue US$m, Revenue from Rechargeable Battery and Photovoltaic, Share of Revenue from Rechargeable Battery and Photovoltaic %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.22 BYD Co. Ltd Total Company Revenue 2011-2017 (US$m, AGR %)

Table 13.23 BYD Co. Ltd Revenue from Rechargeable Battery and Photovoltaic 2011-2017 (US$m, AGR %)

Table 13.24 Robert Bosch GmbH Profile 2017 (CEO, Total Company Revenue US$m, Revenue from Energy and Building Technology US$m, Share of Company Sales from Energy and Building Technology %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.25 Robert Bosch GmbH Total Company Revenue 2013-2017 (US$m, AGR %)

Table 13.26 Robert Bosch GmbH Revenue from Energy and Building Technology 2015-2017 (US$m, AGR %)

Table 13.27 ABB Group Profile 2018 (CEO, Total Company Revenue US$m, Revenue from the Electrification Products Market (US$m), Share of Company Sales from Electrification Products Market %, Net Income / Loss US$m, Net Capital Expenditure US$m, Strongest Business Region, Business Segment in the Market, HQ, Founded, No. of Employees, IR Contact, Ticker, Website)

Table 13.28 ABB Group Total Company Sales 2011-2017 (US$m, AGR %)

Table 13.29 ABB Group Sales in the Electrification Products 2015-2017 (US$m, AGR %)

Table 13.30 Other Companies Involved in the Next Generation Energy Storage Technologies Market 2016 (Company, Location)

Table 14.1 Global Next Generation Energy Storage Technologies Market Forecast 2018-2028 (MW, AGR %, CAGR %, Cumulative)

Table 14.2 Global Next Generation Energy Storage Technologies Market Forecast, By Region 2018-2028 ($bn, AGR %, CAGR %, Cumulative)

Table 14.3 Global EST Market Drivers & Restraints

List of Figures

Figure 1.1 Next-Generation Energy Storage Technologies Market Overview

Figure 1.2 Development Stage of Different Energy Storage Technologies

Figure 1.3 The Performance Characteristics of Advanced and Conventional CAES (Lifecycle-Years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 2.1 Energy Storage Technologies Categorisation

Figure 2.2 Electricity Storage Matrix: EST Characteristics and Requirements of Key Applications

Figure 2.3 Global EST Market Structure Overview

Figure 2.4 Global Energy Storage Capacity by EST type (GW) 1996-2015

Figure 2.5 Global Energy Storage Capacity by EST type (GW) 1996-2015

Figure 2.6 Key Next-Generation EST Market Structure Overview

Figure 2.7 EST Overview of Types of Applications

Figure 3.1 Industrial Electricity Price History in France, Germany, Italy, UK, Japan, Canada, Spain and USA 1990-2016 (Pence/kWh)

Figure 3.2 Industrial Electricity Prices for Medium-Sized Industries in European Countries 2004-2016 (EUR/kWh)

Figure 3.3 Industrial Electricity Prices for Medium Sized Industries in Germany, Spain, France and the United Kingdom 2006-2016 (EUR/kWh)

Figure 3.4 Total Public Energy RD&D Spending of IEA Members 2016 (% of Total RD&D Spending on Energy-Related Projects)

Figure 3.5 Evolution of Total Public Energy RD&D Spending by Selected IEA members 2007-2014 ($m)

Figure 3.6 The Scale and Composition of Installed RES capacity in Selected Countries and Regions (GW)

Figure 3.7 Electricity Generated from Renewable Sources, EU 28, 1990-2016 (TWh, % of Consumption)

Figure 3.8 Number of FCEVs expected to operate in the US, South Korea, Japan and Europe, 2020

Figure 3.9 Technology and Innovation Adoption Lifecycle

Figure 4.1 Capacity and growth forecast for Mechanical Storage 2018-2028

Figure 4.2 Main Types of PHS Installations

Figure 4.3 Evolution of Installed Capacity in the Open-Loop, Closed-Loop and Innovative PHS Submarkets (1926-2015, MW)

Figure 4.4 Main Patterns of Innovation in the Global PHS Sector

Figure 4.5 Average Capacity of Existing and Planned PHS Installations (Submarket, MW)

Figure 4.6 The Performance Characteristics of Innovative PHS (Lifecycle-years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 4.7 Main Applications of Innovative PHS

Figure 4.8 Main Competitors of Innovative PHS

Figure 4.9 Key Market Spaces for Innovative PHS

Figure 4.10 Evolution of Installed Capacity in the Innovative PHS Submarket 1966 - 2015 (MW)

Figure 4.11 Total CAPEX on Innovative PHS by National Market (Cumulative $m)

Figure 4.12 Structure of the CAES Market

Figure 4.13 Round-Trip Efficiency of Conventional Diabatic CAES and Advanced CAES (%)

Figure 4.14 The Performance Characteristics of Advanced and Conventional CAES (Lifecycle-years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 4.15 Main Applications of Advanced Compressed Air Energy Storage

Figure 4.16 Main Competitors of Advanced Compressed Air Energy Storage

Figure 4.17 Key Market Spaces for Advanced CAES

Figure 4.18 Installed CAES Capacity by Category: Diabatic and Isothermal (MW, % of total)

Figure 4.19 Anticipated progress of AA-CAES through the pilot stage onto commercialisation (2014-2020)

Figure 4.20 Selection of Stakeholders and Companies Involved in the Advanced Compressed Air Energy Storage Market

Figure 4.21 The Stages Involved in Liquid Air Energy Storage

Figure 4.22 Round-Trip Efficiency of Liquid Air Energy Storage Variants (Standalone, Integrating Waste Heat and Integrating Waste Cold, %)

Figure 4.23 The Performance Characteristics of Liquid Air Energy Storage (Lifecycle-years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 4.24 Main Applications of Liquid Air Energy Storage

Figure 4.25 Main Competitors of Liquid Air Energy Storage

Figure 4.26 Key Market Spaces for Liquid Air Energy Storage

Figure 4.27 The Historic and Expected Development of Liquid Air Energy Storage (Conceptualisation to Commercialisation, 2005-2018)

Figure 4.28 Selection of Stakeholders and Companies Involved in the Liquid Air Energy Storage Market

Figure 5.1 Capacity and growth forecast for Chemical Energy Storage 2018-2028

Figure 5.2 The Fundamentals of Hydrogen Storage and Hydrogen Fuel Cells

Figure 5.3 The Round-Trip Efficiency of Hydrogen Storage by Pathway Variant (Electricity > Gas > Electricity and Heat, Electricity > Gas > Electricity and Electricity > Gas) (%)

Figure 5.4 The Performance Characteristics of Large-Scale Hydrogen Energy Storage Systems and Hydrogen Fuel Cells (Lifecycle-Years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 5.5 Main Applications of Large-Scale Hydrogen Storage Systems and Hydrogen Fuel Cells

Figure 5.6 Main Competitors of Large-Scale Hydrogen Storage Systems

Figure 5.7 Main Competitors of Hydrogen Fuel Cells

Figure 5.8 Key Market Spaces for Hydrogen Storage and Hydrogen Fuel Cells

Figure 5.9 FCEV Fleet in Operation in Leading National and Regional Markets as of 2014

Figure 5.10 Hydrogen Fueling Stations in Operation in Leading National and Regional Markets as of 2014

Figure 5.11 The Main Types of Hydrogen Storage

Figure 5.12 Existing and Planned Hydrogen Infrastructure in Leading Global Markets (Hydrogen Fueling Stations)

Figure 5.13 Existing and Planned Hydrogen Infrastructure in Leading Global Markets (Hydrogen Fueling Stations)

Figure 5.14 Existing and Planned Alternative Fueling Infrastructure in Leading Global Markets (Hydrogen Fueling Stations)

Figure 5.15 Selection of Stakeholders and Companies Involved in the Large-Scale Hydrogen Energy Storage Systems and Hydrogen Fuel Cells Market

Figure 6.1 Variants of SMES technology

Figure 6.2 The Performance Characteristics of Superconducting Magnetic Energy Storage (Lifecycle-Years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 6.3 Main Applications for Superconducting Magnetic Energy Storage

Figure 6.4 Main Competitors of Superconducting Magnetic Energy Storage

Figure 6.5 Key Market Spaces for Superconducting Magnetic Energy Storage

Figure 6.6 Selection of Stakeholders and Companies Involved in the Superconducting Magnetic Energy Storage Market

Figure 7.1 Key Emerging Battery Chemistries

Figure 7.2 Li-air Categorisation by Electrolyte

Figure 7.3 The Performance Characteristics of Lithium-Air Batteries (Lifecycle-years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 7.4 The Performance Characteristics of Lithium-sulphur Batteries (Lifecycle-years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 7.5 Main Types of Applications of Lithium-sulphur Batteries

Figure 7.6 Key Market Spaces for Lithium-Sulphur Batteries

Figure 7.7 Selection of Stakeholders and Companies Involved in the Lithium-sulphur battery Market

Figure 7.8 Selection of Stakeholders and Companies Involved in the Magnesium-Ion Battery Market

Figure 7.9 The Performance Characteristics of Zinc Air (Lifecycle-Years, Efficiency %, Capacity, Maturity) on a Metric Standardised for all Emerging Technologies

Figure 7.10 Main Applications of Zinc Air Batteries

Figure 7.11 Selection of Stakeholders and Companies Involved in the Zinc-Air Battery Market

Figure 8.1 Capacity and growth forecast for Thermal Energy Storage 2018-2028

Figure 11.1 EST Characteristics and Requirements of Key Applications

Figure 11.2 Cost and Backup Time Comparison of Power Quality Energy Storage Technologies Except Pumped Storage (Euro/kWh & hours)

Figure 11.3 Comparison of the Round-trip Efficiency of Key Established and Emerging Energy Storage Technologies (%)

Figure 12.1 Global Next Generation Energy Storage Technologies Market Forecast, By Region 2018-2028

Figure 12.2 Key National Markets Involved in the Development of Next-Generation Energy Storage Technologies

Figure 12.3 Overview of the Key Next-Generation ESTs Under Development in North America

Figure 12.4 Overview of the Key Next-Generation ESTs Under Development in Europe

Figure 12.5 Overview of the Key Next-Generation ESTs Under Development in Asia

Figure 13.1 Johnson Controls Total Company Sales 2011-2017 (US$m, AGR %)

Figure 13.2 Johnson Controls Sales in the Energy Storage Technologies 2011-2017 (US$m, AGR %)

Figure 13.3 LG Chem Ltd. Total Company Revenue 2012-2016 (US$m, AGR %)

Figure 13.4 LG Chem Ltd. Sales in the Energy Storage Technologies Market 2011-2015 (US$m, AGR %)

Figure 13.5 Duke Energy Corporation Total Company Revenue 2011-2017 (US$m, AGR %)

Figure 13.6 Duke Energy Corporation Revenues in the Energy Storage Technologies Market 2014-2017 (US$m, AGR %)

Figure 13.7 NextEra Energy, Inc. operating Revenue 2011-2017 (US$m, AGR %)

Figure 13.8 NextEra Energy, Inc. Sales in the Renewable Technologies Market 2012-2017 (US$m, AGR %)

Figure 13.9 Edison International Total Company Sales 2011-2017 (US$m, AGR %)

Figure 13.10 Samsung SDI Co. Ltd. Total Company Revenue 2011-2017 (US$m, AGR %)

Figure 13.11 Samsung SDI Co. Ltd. Revenue from LI-Ion Market 2014-2016 (US$m, AGR %)

Figure 13.12 Mitsubishi Electric Corporation Total Company Sales 2011-2017 (US$m, AGR %)

Figure 13.13 Mitsubishi Electric Corporation Revenue from Energy and Electric Systems 2011-2017 (US$m, AGR %)

Figure 13.14 BYD Co. Ltd Total Company Revenue 2011-2017 (US$m, AGR %)

Figure 13.15 BYD Co. Ltd Revenue from Rechargeable Battery and Photovoltaic 2011-2017 (US$m, AGR %)

Figure 13.16 Robert Bosch GmbH Total Company Revenue 2013-2017 (US$m, AGR %)

Figure 13.17 Robert Bosch GmbH Revenue from Energy and Building Technology (2015-2017 (US$m)

Figure 13.18 ABB Group Total Company Sales 2011-2017 (US$m, AGR%)

Figure 13.19 ABB Group Revenue in the Electrification Products Market (US$m, AGR %)

Figure 14.1 Next-Generation Energy Storage Technologies Market Overview

Figure 14.2 Development Stage of Different Energy Storage Technologies

Figure 14.3 Anticipated progress of AA-CAES through the pilot stage onto Commercialisation (2014-2020)

Figure 14.4 The Historic Development of Liquid Air Energy Storage (Conceptualisation to Commercialisation, 2005-2018)

Figure 14.5 Existing and Planned Hydrogen Infrastructure in Leading Global Markets (Hydrogen Fueling Stations)