Visiongain has calculated that the LNG infrastructure market will see a total expenditure of $63,606 mn in 2017, including both Liquefaction and Regasification.

Read on to discover the potential business opportunities available.

LNG is used in various sectors such as automobile, industrial, and commercial. It is becoming a popular energy source due to its high replacement potential, considering its environmental benefits over other energy sources. The major advantage of LNG is the low emission of CO2, which makes it an efficient alternative to conventional fossil fuels. These advantages have been driving LNG demand from the industrial as well as automobile sector. Simultaneously, it is boosting the development of large-scale LNG terminals across the globe.

Increasing utilization of natural gas over oil is one of the major drivers for the large-scale terminals market. Various companies are focusing on establishing more liquefaction and regasification terminals in offshore areas to fulfil the increasing demand of LNG. In the current scenario, the overall global outlook is gradually shifting towards utilization of cleaner fuels. Natural gas is expected to occupy a major share of primary energy consumption by the end of the forecast period. With a boom in LNG trade activities expected in the future and steadily growing consumption pattern in emerging nations in Asia Pacific, an upward pressure on large-scale LNG sector development activities is inevitable in the future.

The construction of large-scale onshore liquefaction and regasification terminals is a function of the development of the global LNG industry. Investment in such infrastructure is dictated by unique supply and demand circumstances in different geographies, such as the US unconventional oil and gas boom and economic growth in Asia, particularly China.

There are a number of exciting LNG liquefaction prospects around the world in 2016, both under construction and perspective. The question is whether the demand of East Asia will be strong enough to support the economics of an abundant supply of liquefaction opportunities. The decline of the US as an import market for LNG has troubled financiers but has been balanced by demand in Asia, East Asia and emerging demand in South America.

Visiongain’s LNG infrastructure market report can keep you informed and up to date with the developments in the Liquefication Market in Australia, Canada, US and East Africa and Rest of the World. Visiongain has also included in-Depth market analysis about the Regasification markets in China, Japan, South Korea, India and Europe.

With reference to this report, it details the key investments trend in the global market, subdivided by regions, capital expenditure and capacity. Through extensive secondary research and interviews with industry experts, visiongain has identified a series of market trends that will impact the LNG infrastructure market over the forecast timeframe.

The report will answer questions such as:

– What are the key trends and factors affecting spending on new liquefaction infrastructure?

– What factors dictate this investment?

– How are the economics of terminals shaping up?

– What is the interplay between expenditure on regasification terminals and liquefaction capacity?

– How are demand markets for LNG most likely to evolve, and why?

– Who will be the main exporters and importers of LNG over the next decade?

– How will the future global LNG trade routes change?

– How much extra LNG capacity will enter the global market over the next decade

Five Reasons Why You Must Order and Read This Report Today:

1) The report provides CAPEX and capacity forecasts and analyses for the 5 Leading Regional Players in the LNG Liquefaction Market 2017-2027

– Australia

– Canada

– East Africa

– Russia

– US

– Rest of the World (Includes Iran, Papua New Guinea, Qatar, Trinidad & Tobago, Algeria, Angola & Nigeria)

2) The report provide CAPEX and capacity forecasts and analyses for the 5 Leading Regional Players in the LNG Regasification Market 2017-2027

– China

– Europe

– Japan

– South Korea

– India

3) The report includes tables of all currently operating, under construction and planned liquefaction and regasification facilities, listing their Location, Operational Year, Status, Capacity, Owner(s) and EPC Cost

4) The analysis is underpinned by our exclusive interviews with leading experts from:

– Linde AG

5) The report provides detailed profiles of the leading companies operating within the LNG Infrastructure market:

– BHP Billiton

– ExxonMobil

– BP

– ConocoPhillips.

– Total S.A

– Linde AG

– Royal Dutch Shell

– PETRONAS

– Chevron Corporation

– Rosneft

This independent 328-page report guarantees you will remain better informed than your competitors. With 156 tables and figures examining the LNG Infrastructure market space, the report gives you a direct, detailed breakdown of the market. PLUS, capital expenditure AND capacity AND tables of all currently operating, under construction and planned liquefaction and regasification facilities, as well as in-Depth analysis, from 2017-2027 will keep your knowledge that one step ahead of your rivals.

This report is essential reading for you or anyone in the LNG sectors. Purchasing this report today will help you to recognise those important market opportunities and understand the possibilities there. I look forward to receiving your order.

Visiongain is a trading partner with the US Federal Government

CCR Ref number: KD4R6

1. Report Overview

1.1 Liquefied Natural Gas (LNG)Infrastructure Market Overview

1.2 Market Structure Overview and Market Definition

1.3 Why You Should Read This Report

1.4 How This Report Delivers

1.5 Key Questions Answered by This Analytical Report Include:

1.6 Who is This Report For?

1.7 Methodology

1.7.1 Primary Research

1.7.2 Secondary Research

1.7.3 Market Evaluation & Forecasting Methodology

1.8 Frequently Asked Questions (FAQ)

1.9 Associated Visiongain Reports

1.10 About Visiongain

2. Introduction to The Liquefied Natural Gas (LNG) Infrastructure Market

2.1 Global LNG Infrastructure Market Structure

2.2 Market Definition

2.3 LNG Industry Outlook

2.4 LNG- Value Chain Analysis

2.5 The Role and Function of LNG Infrastructure

2.6 What is Natural Gas Liquefaction?

2.7 What is LNG Regasification?

2.8 Brief History of LNG Infrastructure

3. Global Overview of Liquefied Natural Gas (LNG) Infrastructure Market 2017-2027

3.1 Global Overview

3.2 Global Liquefied Natural Gas (LNG) Import Terminals

3.2 Global Liquefied Natural Gas (LNG) Export Terminals

4. Liquefied Natural Gas (LNG) Infrastructure Submarkets Forecasts 2017-2027

4.1 Global Liquefied Natural Gas (LNG) Infrastructure Submarkets Forecasts, by Type 2017-2027

4.1.1 Global Liquefaction Liquefied Natural Gas (LNG) Infrastructure Forecasts 2017-2027

4.1.2 Global Regasification Forecasts 2017-2027

4.1.3 Global Liquefied Natural Gas (LNG) Infrastructure, by Liquefied Natural Gas (LNG) Infrastructure Type Drivers and Restraints

4.2 Demand Side Factors

4.3 Supply-Side Drivers

4.4 Global LNG Market: Where Are We Now; Where Will We Be in 5 Years; Where Will We Be in 10 Years?

4.5 Oil Price Analysis

4.6 Supply-Side Factors

4.7 Demand-Side Factors

4.8 Other Major Variables that Impact the Oil Price

4.9 Oil Price and LNG Price Relationship

4.10 Towards an Oversupplied LNG Market

4.11 Large-Scale Liquefaction Terminals in Operation, Under Construction and Planned

4.12 Large-Scale Regasification Terminals in Operation, Under Construction and Planned

5. The Leading Regional Players in LNG Liquefaction Market (Large-Scale Onshore) 2017-2027

5.1 Australian Large-Scale Onshore LNG Liquefaction Market 2017-2027

5.1.1 Overall Drivers & Restraints on Australian LNG Liquefaction Investment

5.1.2 Capital Expenditure Analysis

5.1.3 What Are the Prospects for Brownfield Terminal Development?

5.1.4 Future Outlook for Australian LNG Infrastructure

5.2 U.S. Large-Scale Onshore LNG Liquefaction Market 2017-2027

5.2.1 Overall Drivers & Restraints on U.S. LNG Liquefaction Investment

5.2.2 Capital Expenditure Analysis

5.2.2.1 Drivers for Capital Expenditure

5.2.2.2 Restraints on Capital Expenditure

5.2.3 US Large-Scale Onshore LNG Liquefaction Terminal Locations

5.3 Russian Large-Scale Onshore LNG Liquefaction Market 2017-2027

5.3.1 Overall Drivers & Restraints on RUSSIAN LNG Liquefaction Investment

5.3.2 Russia Onshore Liquefaction Facilities and Prospects

5.4 Canadian Large-Scale Onshore LNG Liquefaction Market 2017-2027

5.4.1 Overall Drivers & Restraints on Canadian LNG Liquefaction Investment

5.4.2 Capital Expenditure Analysis

5.4.3 Canadian Onshore LNG Liquefaction Projects

5.4.4 Greenfield Terminal Costs and Economic

5.4.5 Threats to LNG Liquefaction Terminal Investment

5.5 East African Large-Scale Onshore LNG Liquefaction Market 2017-2027

5.5.1 Overall Drivers & Restraints on East African LNG Liquefaction Investment

5.5.2 Mozambique LNG Liquefaction Outlook

5.5.3 Upstream Assets Relevant to LNG Liquefaction Development

5.5.4 Anadarko’s LNG Plan: The Onshore Option

5.5.5 ENI’s FLNG Option

5.5.6 Mozambique Development Context& Tax Regime

5.5.7 Most Likely Scenario for Mozambique LNG Development

5.5.8 Tanzanian LNG Liquefaction Outlook

5.5.9 Shell’s Acquisition of BG Group in 2015

5.5.10 Tanzania Development Context & Tax Regime

5.6 Rest of the World Large-Scale Onshore LNG Liquefaction Market 2017-2027

5.6.1 Iranian Onshore LNG Liquefaction Prospects

5.6.2 Joint LNG Exports

5.6.3 Potential Export Markets

5.6.4 Domestic Situation

5.6.5 Papua New Guinea Onshore LNG Liquefaction Prospects

5.6.6 Qatari Onshore LNG Liquefaction Prospects

5.6.7 Trinidad & Tobago Onshore LNG Prospects

5.6.8 Algeria

5.6.9 Angola

5.6.10 Nigeria

6. The Leading Regional Players in LNG Regasification Market (Large-Scale Onshore) 2017-2027

6.1 China Large-Scale Onshore LNG Regasification Market 2017-2027

6.1.1 Overall Drivers & Restraints on China LNG Regasification Investment

6.1.2 Domestic Supply – Shale Gas Development

6.1.3 Domestic Supply – Coalbed Methane Development

6.1.4 Domestic Supply – Tight Gas Development

6.1.5 Imports of Pipeline Gas

6.2 Japan Large-Scale Onshore LNG Regasification Market 2017-2027

6.2.1 Overall Drivers & Restraints on Japan LNG Regasification Investment

6.2.2 Capital Expenditure Analysis

6.2.3 Restarting Nuclear Power Generation

6.2.4 The Future of Coal Power Generation

6.2.5 Liquefaction Equity Investment Indicative of Future Imports

6.3 India Large-Scale Onshore LNG Regasification Market 2017-2027

6.3.1 Overall Drivers & Restraints on India LNG Regasification Investment

6.3.2 Indian LNG Infrastructure Outlook

6.3.4 LNG Pricing

6.4 Europe Large-Scale Onshore LNG Regasification Market 2017-2027

6.4.1 Overall Drivers & Restraints on Europe LNG Regasification Investment

6.4.2 How Does the Ukraine Crisis Impact Future European LNG

6.4.3 The Impact of Gas Pipeline Developments on LNG Infrastructure Investment

6.4.4 The Economics of LNG Imports vs Russian Gas

6.4.5 The FSRU Option – A Threat to Onshore Regasification in Europe?

6.4.6 What Will the Effect of UK North Sea Gas Declines be on Regasification Infrastructure?

6.4.7 Shale Gas Development Issues and their Relation to LNG Infrastructure Development

6.4.8 Poland

6.4.9 UK

6.4.10 Energy Security & Geo-Politics as a Driver of Regasification Infrastructure Development

6.4.11 A Shift to Natural Gas Power Generation?

6.4.12 Baltic States LNG Regasification Outlook

6.4.13 Italian LNG Regasification Terminal Outlook

6.5 South Korea Large-Scale Onshore LNG Regasification Market 2017-2027

6.5.1 Overall Drivers & Restraints on South Korea LNG Regasification Investment

6.5.2 Current LNG Demand Situation

6.5.3 What is the Future of Nuclear Power Generation in South Korea?

6.6 Rest of the World Large-Scale Onshore LNG Regasification Market 2017-2027

6.6.1 Overall Drivers & Restraints on Rest of the World LNG Regasification Investment

6.6.2 South & Central America

6.6.3 The Middle East& Africa

7. PESTEL Analysis of the LNG Infrastructure Market

7.1 PESTEL Analysis

8. Expert Opinion

8.1 Primary Correspondents

8.2 Global LNG Infra Market Outlook

8.3 Driver & Restraints

8.4 Dominant Region/Country in the LNG Liquefaction Market

8.5 Dominant Region/Country in the LNG Regasification Market

8.6 By type (Liquefaction & Regas) Market Scenario

8.7 Overall Growth Rate, Globally

9. Leading Companies in LNG Infrastructure Market

9.1 BHP Billiton

9.2 ExxonMobil

9.3 BP P.L.C.

9.4 ConocoPhillips

9.5 Total S.A.

9.6 Linde AG

9.7 Royal Dutch Shell

9.8 PETRONAS

9.9 Chevron Corporation

9.10 Rosneft

10. Conclusion & Recommendations

10.1 Key Findings

10.2 Recommendations

11. Glossary

Appendix

Associated Visiongain Reports

Visiongain Report Sales Order Form

Appendix A

Appendix B

Visiongain Report Evaluation Form

List of Tables

Table 1.1 Global LNG Infrastructure Market by Regional Market Forecast 2017-2027 ($ mn/MMTPA, AGR %, CAGR)

Table 3.1 Global Liquefaction Liquefied Natural Gas (LNG) Infrastructure Forecast 2017-2027($mn, AGR %, CAGR %, Cumulative)

Table 3.2 Global Liquefied Natural Gas (LNG) Import Terminals Details (Region, Country, Project, Onshore / Offshore, Status, Startup, Operator, Capacity mt/y)

Table 3.3 Global Liquefied Natural Gas (LNG) Export Terminals (Region, Country, Project, Onshore / Offshore, Status, Startup, Operator, Capacity mt/y, Storage '000cm)

Table 4.1 Global Liquefied Natural Gas (LNG) Infrastructure Market Forecast Liquefaction vs. Regasification 2017-2027($mn, AGR %, Cumulative)

Table 4.2 Global Liquefied Natural Gas (LNG) Infrastructure Market Forecast Liquefaction vs. Regasification 2017-2027(MMTPA, AGR %, Cumulative)

Table 4.3 Global Liquefaction Liquefied Natural Gas (LNG) Infrastructure Forecast 2017-2027($mn, AGR %, CAGR %, Cumulative)

Table 4.4 Global Regasification Forecast 2017-2027($mn, AGR %, CAGR %, Cumulative)

Table 4.5 Global Liquefaction Natural Gas (LNG) Infrastructure Drivers and Restraints

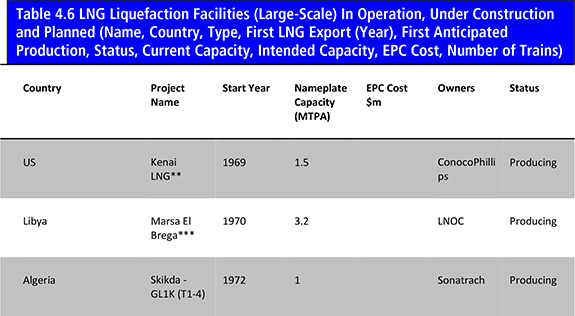

Table 4.6 LNG Liquefaction Facilities (Large-Scale) In Operation, Under Construction and Planned (Name, Country, Type, First LNG Export (Year), First Anticipated Production, Status, Current Capacity, Intended Capacity, EPC Cost, Number of Trains)

Table 4.7 Large-Scale Regasification Terminals in Operation, Under Construction and Planned (Country, Terminal Name, Start Year, Nameplate Receiving Capacity (MTPA), EPC Cost $m, Owners, Status)

Table 5.1 Global LNG Liquefaction Market, by Country/Region Forecast CAPEX 2017-2027 ($mn, AGR %, Cumulative)

Table 5.2 Global LNG Liquefaction Market, by Country/Region Forecast Capacity 2017-2027 (MMTPA, AGR %, Cumulative)

Table 5.3 Australian Large-Scale Onshore LNG Liquefaction Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 5.4 Australian Large-Scale Onshore LNG Liquefaction Drivers and Restraints

Table 5.5 U.S. Large-Scale Onshore LNG Liquefaction Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 5.6 U.S. Large-Scale Onshore LNG Liquefaction Drivers and Restraints

Table 5.7 Russian Large-Scale Onshore LNG Liquefaction Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 5.8 Russian Large-Scale Onshore LNG Liquefaction Drivers and Restraints

Table 5.9 Canadian Large-Scale Onshore LNG Liquefaction Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 5.10 Canadian Large-Scale Onshore LNG Liquefaction Drivers and Restraints

Table 5.11 East African Large-Scale Onshore LNG Liquefaction Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 5.12 East African Large-Scale Onshore LNG Liquefaction Drivers and Restraints

Figure 5.13 Mozambique Gas Blocks Relevant to LNG Exports (Operator, Block, Onshore/Offshore, km2, Project Shareholders, Status)

Table 5.14 Rest of the World Large-Scale Onshore LNG Liquefaction Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.1 Global LNG Regasification Market, by Country/Region Forecast CAPEX 2017-2027 ($mn, AGR %, Cumulative)

Table 6.2 Global LNG Regasification Market, by Country/Region Forecast Capacity 2017-2027 (MMTPA, AGR %, Cumulative)

Table 6.3 China Large-Scale Onshore LNG Regasification Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.4 China Large-Scale Onshore LNG Regasification Drivers and Restraints

Table 6.5 Japan Large-Scale Onshore LNG Regasification Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.6 Japan Large-Scale Onshore LNG Regasification Drivers and Restraints

Table 6.7 India Large-Scale Onshore LNG Regasification Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.8 India Large-Scale Onshore LNG Regasification Drivers and Restraints

Table 6.9 Europe Large-Scale Onshore LNG Regasification Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.10 Europe Large-Scale Onshore LNG Regasification Drivers and Restraints

Table 6.11 South Korea Large-Scale Onshore LNG Regasification Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.12 South Korea Large-Scale Onshore LNG Regasification Drivers and Restraints

Table 6.13 Rest of the World Large-Scale Onshore LNG Regasification Facility CAPEX & Capacity 2017-2027 ($m, MMTPA, AGR %, Cumulative)

Table 6.14 Rest of the World Large-Scale Onshore LNG Regasification Drivers and Restraints

Table 7.1 PESTEL Analysis, LNG Infrastructure Market

Table 9.1 BHP Billiton Profile 2016 (Market Entry, Public/Private, Headquarter, No. of Employees), Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Listed on & Products/Services

Table 9.2 BHP Billiton, Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.3 ExxonMobil Profile 2016 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.4 ExxonMobil, Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.5 BP P.L.C. (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.6 BP P.L.C., Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.7 ConocoPhillips Profile 2016 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.8 ConocoPhillips Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.9 Total S.A., Profile 2016 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.10 Total S.A., Inc. Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.11 Linde AG Company Profile 2015 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.12 Linde AG Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.13 Royal Dutch Shell Profile 2016 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.14 Royal Dutch Shell, Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.15 PETRONAS Profile 2015 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.16 PETRONAS Total Company Revenue 2011-2015 ($bn, AGR %)

Table 9.17 Chevron Corporation Profile 2015 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.18 Chevron Corporation, Total Company Sales 2012-2016 ($bn, AGR %)

Table 9.19 Rosneft Profile 2015 (Market Entry, Public/Private, Headquarter, No. of Employees, Revenue 2016 ($bn), Change in Revenue, Geography, Key Market, Company Sales from LNG Infrastructure Market, Listed on & Products/Services

Table 9.20 Rosneft Total Company Sales 2012-2016 ($bn, AGR %)

List of Figures

Figure 1.1 Global Natural Gas Consumption Forecast 2010-2035

Figure 1.2 The LNG Liquefaction Market by Country/Region Market Share Forecast 2017, 2022, 2027 (% Share)

Figure 2.1 Global LNG Infrastructure Market Segmentation Overview

Figure 2.2 LNG, Value Chain Analysis

Figure 2.3 LNG Supply Chain from Field Production to Gas Grid

Figure 2.4 Simplified Flow Diagram of the Liquefaction Process

Figure 2.5 LNG Industry Brief Early History Timeline

Figure 3.1 Global Liquefied Natural Gas (LNG) Infrastructure Forecast 2017-2027 ($mn, AGR %)

Figure 4.1 Global Liquefied Natural Gas (LNG) Infrastructure Submarket Forecast 2017-2027 ($mn)

Figure 4.2 Global Liquefied Natural Gas (LNG) Infrastructure Market by Type (CAPEX) Share Forecast 2017, 2022, 2027 (% Share)

Figure 4.3 Liquefied Natural Gas (LNG) Infrastructure Market, By Liquefaction Forecast 2017-2027 ($mn, AGR%)

Figure 4.4 Liquefied Natural Gas (LNG) Infrastructure Market, By Regasification Forecast 2017-2027 ($mn, AGR%)

Figure 4.5 Top 10 LNG Exporter Countries (Million Tons), 2016

Figure 4.6 WTI, Brent, Dubai, Nigerian Forcados Oil Prices 2000-2016 ($/bbl)

Figure 5.1 Regional LNG Liquefaction Market, by CAPEX 2017-2027

Figure 5.2 Regional LNG Liquefaction Market, By Capacity (MMTPA) 2017-2027

Figure 5.3 Leading Country/Regional LNG Liquefaction Market Share by CAPEX 2017

Figure 5.4 Leading Country/Regional LNG Liquefaction Market Share by CAPEX 2022

Figure 5.5 Leading Country/Regional LNG Liquefaction Market Share 2027

Figure 5.6 Australian Large-Scale Onshore LNG Liquefaction Facility Forecast 2017-2027 ($mn, AGR%)

Figure 5.7 Australian Large-Scale Onshore LNG Liquefaction Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 5.8 Australian Large-Scale Onshore LNG Liquefaction Facility, by Capacity Forecast 2017-2027

Figure 5.9 Australian Onshore LNG Liquefaction Facility Cost per mmtpa of Capacity (Greenfield Terminals, CAPEX per mmtpa ($mn)

Figure 5.10 U.S. Large-Scale Onshore LNG Liquefaction Facility Forecast 2017-2027 ($mn, AGR%)

Figure 5.11 U.S. Large-Scale Onshore LNG Liquefaction Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 5.12 U.S. Large-Scale Onshore LNG Liquefaction Facility, by Capacity Forecast 2017-2027

Figure 5.13 USLNG Export Terminals Currently Approved by FERC (Name, Location, Sponsor)

Figure 5.14 USLNG Export Terminals Proposed to FERC (Name, Location, Sponsor)

Figure 5.15 Russian Large-Scale Onshore LNG Liquefaction Facility Forecast 2017-2027 ($mn, AGR%)

Figure 5.16 Russian Large-Scale Onshore LNG Liquefaction Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 5.17 Russian Large-Scale Onshore LNG Liquefaction Facility, by Capacity Forecast 2017-2027

Figure 5.18 Onshore LNG Liquefaction Facility Cost per mmtpa of Capacity (Greenfield Terminals, CAPEX per mmtpa ($m))

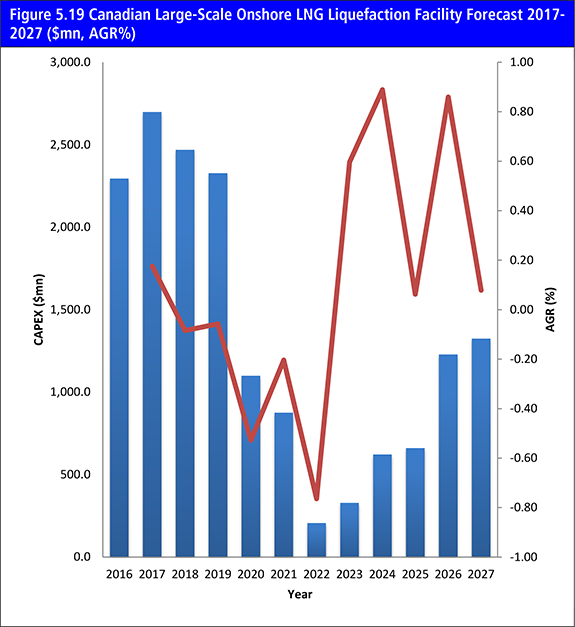

Figure 5.19 Canadian Large-Scale Onshore LNG Liquefaction Facility Forecast 2017-2027 ($mn, AGR%)

Figure 5.20 Canadian Large-Scale Onshore LNG Liquefaction Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 5.21 Canadian Large-Scale Onshore LNG Liquefaction Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 5.22 East African Large-Scale Onshore LNG Liquefaction Facility Forecast 2017-2027 ($mn, AGR%)

Figure 5.23 East African Large-Scale Onshore LNG Liquefaction Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 5.24 East African Large-Scale Onshore LNG Liquefaction Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 5.25 Rest of the World Large-Scale Onshore LNG Liquefaction Facility Forecast 2017-2027 ($mn, AGR%)

Figure 5.26 Rest of the World Large-Scale Onshore LNG Liquefaction Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 5.27 Rest of the World Large-Scale Onshore LNG Liquefaction Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 5.28 North Field, Qatar

Figure 6.1 Regional LNG Regasification Market by CAPEX 2017-2027

Figure 6.2 Regional LNG Regasification Market By Capacity (MMTPA) 2017-2027

Figure 6.3 Leading Country/Regional LNG Regasification Market Share by CAPEX 2017

Figure 6.4 Leading Country/Regional LNG Regasification Market Share by CAPEX 2022

Figure 6.5 Leading Country/Regional LNG Regasification Market Share 2027

Figure 6.6 China Large-Scale Onshore LNG Regasification Facility Forecast 2017-2027 ($mn, AGR%)

Figure 6.7 China Large-Scale Onshore LNG Regasification Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 6.8 China Large-Scale Onshore LNG Regasification Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 6.9 Japan Large-Scale Onshore LNG Regasification Facility Forecast 2017-2027 ($mn, AGR%)

Figure 6.10 Japan Large-Scale Onshore LNG Regasification Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 6.11 Japan Large-Scale Onshore LNG Regasification Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 6.12 Japanese Net Electricity Generation by Fuel Type, 2013 & 2030 Target (% of TWh)

Figure 6.13 India Large-Scale Onshore LNG Regasification Facility Forecast 2017-2027 ($mn, AGR%)

Figure 6.14 India Large-Scale Onshore LNG Regasification Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 6.15 India Large-Scale Onshore LNG Regasification Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 6.16 Europe Large-Scale Onshore LNG Regasification Facility Forecast 2017-2027 ($mn, AGR%)

Figure 6.17 Europe Large-Scale Onshore LNG Regasification Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 6.18 Europe Large-Scale Onshore LNG Regasification Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 6.19 UK Natural Gas Consumption & Production, 2000-2024 (bcm/a)

Figure 6.20 South Korea Large-Scale Onshore LNG Regasification Facility Forecast 2017-2027 ($mn, AGR%)

Figure 6.21 South Korea Large-Scale Onshore LNG Regasification Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 6.22 South Korea Large-Scale Onshore LNG Regasification Facility, by Capacity Forecast 2017-2027(MMTPA)

Figure 6.23 Rest of the World Large-Scale Onshore LNG Regasification Facility Forecast 2017-2027 ($mn, AGR%)

Figure 6.24 Rest of the World Large-Scale Onshore LNG Regasification Facility Share Forecast 2017, 2022, 2027 (% Share)

Figure 6.25 Rest of the World Large-Scale Onshore LNG Regasification Facility, by Capacity Forecast 2017-2027 (MMTPA)

Figure 9.1 BHP Billiton, Revenue, ($bn& AGR %), 2012-2016

Figure 9.2 BHP Billiton Revenue % Share by Geographic Segment, 2016

Figure 9.3 BHP Billiton Revenue % Share by Business Segment, 2016

Figure 9.4 ExxonMobil, Revenue, ($bn& AGR %), 2012-2016

Figure 9.5 BP P.L.C., Revenue, ($bn& AGR %), 2012-2016

Figure 9.6 BP P.L.C. Revenue % Share by Geographic Segment, 2016

Figure 9.7 BP P.L.C. Revenue % Share by Business Segment, 2016

Figure 9.8 ConocoPhillips, Revenue, ($bn& AGR %), 2012-2016

Figure 9.9 ConocoPhillips Revenue % Share by Product Segment, 2016

Figure 9.10 ConocoPhillips Revenue % Share by Regional Segment, 2016

Figure 9.11 Total S.A., Inc. Revenue, ($bn& AGR %), 2012-2016

Figure 9.12 Total S.A. Revenue % Share by Business Segment, 2016

Figure 9.13 Linde AG, Revenue, ($bn& AGR %), 2012-2016

Figure 9.14 Linde AG Revenue % Share by Business Segment, 2016

Figure 9.15 Linde AG Revenue % Share by Regional Segment (Gases Division), 2016

Figure 9.16 Royal Dutch Shell Revenue ($bn& AGR %), 2012-2016

Figure 9.17 Royal Dutch Shell Revenue % Share by Geographic Segment, 2016

Figure 9.18 Royal Dutch Shell Revenue % Share by Business Segment, 2016

Figure 9.19 PETRONAS Total Company Revenue ($bn & AGR %), 2011-2015

Figure 9.20 PETRONAS Revenue % Share by Product Segment, 2015

Figure 9.21 PETRONAS Revenue % Share by Geographical Trade, 2015

Figure 9.22 PETRONAS Revenue % Share by Business Segment, 2015

Figure 9.23 PETRONAS Revenue % Share by Geographic Segment, 2015

Figure 9.24 Chevron Corporation, Revenue, ($bn& AGR %), 2012-2016

Figure 9.25 Chevron Corporation Revenue % Share by Business Segment, 2016

Figure 9.26 Rosneft Revenue ($bn& AGR %), 2013-2016

Figure 9.27 Rosneft % Share by Business Segment, 2016

Figure 10.1 Global Liquefaction LNG Infrastructure Market Forecast 2017-2027 ($ mn, AGR %)

Figure 10.2 Global Regasification LNG Infrastructure Market Forecast 2017-2027 ($ mn, AGR %)