The Brazilian Pharmaceutical market was valued at $26.40bn in 2016. Visiongain forecasts this market to increase at a CAGR of 7.6% in the first half of the forecast period. Originator drugs held the largest market share in 2016, this trend however will change in the second half of the forecast period where we predicted that Generic drugs will take over the lead.

How this report will benefit you

Read on to discover how you can exploit the future business opportunities emerging in this sector.

In this brand new report you find 181-page report you will receive 107 charts – all unavailable elsewhere.

The 181-page report provides clear detailed insight into the Brazilian Pharmaceutical market. Discover the key drivers and challenges affecting the market.

By ordering and reading our brand new report today you stay better informed and ready to act.

Report Scope

• Brazilian Pharmaceutical Market forecasts from 2017-2027

• Brazilian Pharmaceutical Market forecasts from 2017-2027, by segment:

• Originator Drugs

• Generic Drugs

• OTC

• Brazilian Pharmaceutical Market forecasts from 2017-2027, by therapeutic area:

• CNS

• Cardiovascular

• Gastrointestinal/Metabolic

• Oncology

• Infectious Disease

• Leading Domestic Companies in the Brazilian Pharmaceutical Market:

• EMS

• Hypermarcas

• Medley

• Eurofarma

• Aché

• Cristalia

• Teuto

• Libbs

• Biolab

• União Química

• Leading Multinational Companies in the Brazilian Pharmaceutical Market:

• Novartis

• Sanofi

• Roche

• Merck & Co.

• Pfizer

• Takeda

• Bayer

• GlaxoSmithKline

• Boehringer Ingelheim

• Astra Zeneca

• SWOT and STEP Analysis of the Brazilian Pharmaceutical market

• This report also discusses:

• The Brazilian healthcare environment, covering important institutional bodies and agencies, surveying the regulatory system, analyzing the balance between public and private healthcare provision and looking at the wholesale and distribution landscape

• Regional variations within Brazil, with profiles of each region and an analysis of their healthcare challenges and opportunities

• Brazilian Biologics Market, which includes qualitative and quantitative analysis.

Visiongain’s study is intended for anyone requiring commercial analyses for the Brazilian Pharmaceutical market and the leading companies competing in that country. You find data, trends and predictions.

Buy our report today Brazilian Pharmaceutical Market Outlook 2017-2027: Originator, Generic, OTC, CNS, Cardiovascular, Gastrointestinal, Metabolic, Oncology, Infectious Diseases, Domestic Manufacturers and International Drug Companies.

Visiongain is a trading partner with the US Federal Government

CCR Ref number: KD4R6

1. Report Overview

1.1 Brazil: Pharmaceutical Market Overview

1.2 Brazilian Pharmaceutical Market Segmentation

1.3 Why You Should Read This Report

1.4 How This Report Delivers

1.5 Main Questions Answered by This Survey

1.6 Who is Our Report For?

1.7 Research and Analysis Methods

1.8 Frequently Asked Questions (FAQs)

1.9 Some Associated Reports

1.10 About Visiongain

2. Introduction to the Brazilian Pharmaceutical Market

2.1 The Brazilian Pharmaceutical Market Overview

2.2 Generics Segment Continues to Grow in Importance

2.3 Central Nervous System Related Disorders– The Largest Therapeutic Area in 2016

2.4 Four Domestic Companies in the Top Ten in 2016

3. The Significance of the Brazilian Market

3.1 Brazilian Economy is the Eight Largest in the World

3.2 Brazil is the Eighth Largest Pharmaceutical Market

3.3 Brazil is the Largest Market in Latin America

3.4 Brazil Qualifies as a ‘Pharmerging’ Country and one of the BRIC Markets

4. Organisation of the Brazilian Pharmaceutical Market

4.1 ANVISA – Brazil’s Equivalent of the FDA

4.2 Other Influential Organisations

4.3 SUS – One of the World’s Largest Public Health Systems

4.4 Private Healthcare Accessed by 25% of the Population

4.5 Private Insurance Market Growing but Costs are Rising

4.6 New Drug Price Adjustment System Introduced

4.7 RENAME Drug Reimbursement System and the Farmácia Popular

4.8 Extensive Network of Pharmacies in Brazil

4.9 Wholesale and Retail Sectors Undergoing Consolidation

4.10 Panpharma is the Top Wholesale Distributor

4.11 Profarma is the Largest Mixed Distributor

4.12 Raia Drogasil is the Leader in the Retail Sector

4.13 Spending on Marketing Approaches $5bn

5. Major Differences in Healthcare Between Regions

5.1 Size and Prosperity of Different Regions

5.2 South-East is the Richest and Most Populous Region

5.3 South Has the Second Highest GDP

5.4 North-East Has the Second Highest Pharmaceutical Market Share

5.5 North is the Largest and Poorest Region

5.6 Mid-West is a Landlocked Region Housing the Nation’s Capital

6. Product Segments in the Brazilian Pharmaceutical Market 2016-2027

6.1 Forecasts for the Originator, Generic and OTC Segments 2016-2027

6.2 Originator Segment Will be Overtaken by Generics

6.2.1 Product Development Partnerships to Reduce Costs

6.2.2 Originator Drugs Threatened by 35% Cheaper Generics

6.3 Generics Drug Segment Forecast 2016-2027 – Continued Rapid Growth

6.3.1 Rapid Expansion of Generic Segment

6.3.2 Generic Companies Aiming for 45% Market Share

6.3.3 Similares Drugs Face Same Pricing Rules as Generics

6.3.4 Counterfeit Drugs Account for 20% of the Market

6.3.5 National Drug Security System to Tackle Counterfeit Drugs

6.3.6 Challenges for the Brazilian Generics Market

6.4 Brazilian Biologics Market

6.4.1 Biosimilars Market to Double in Size by 2017

6.4.2 BiocadBrazil Brings More Biosimilars to Brazil

6.5 OTC Drug Segment Forecast 2016-2027

6.5.1 Analgesics and Multivitamins Favoured by Brazilians

6.5.2 One Sixth of Population Buy Multivitamins

6.5.3 Restrictions on OTC Products Reversed

6.5.4 Consumer Health Treatments Remain Prominent in the Market

7. Therapeutic Areas of the Brazilian Market, 2016-2027

7.1 Forecasts for CNS, Cardiovascular, Gastrointestinal/Metabolic, Oncology, Infectious Diseases and Other Therapeutic Areas, 2016-2027

7.2 The Rise of Non-Communicable Diseases

7.3 Market Forecast for CNS Conditions 2016-2027

7.3.1 CNS Conditions Currently the Largest Therapeutic Area

7.3.2 Domestic Companies Target Generic and OTC CNS Products

7.3.3 Foreign Companies Target Analgesics Market

7.3.4 One Fifth of Brazilians Have Suffered Depression

7.3.5 CNS Conditions: Drivers and Restraints

7.4 Market Forecast for Cardiovascular Therapeutic Area, 2016-2027

7.4.1 Rate of Cardiovascular Disease Expected to Triple

7.4.2 Almost One Quarter of the Population are Hypertensive

7.4.3 Statin Revenues Decline with Loss of Patent Protection

7.4.4 Domestic and International Companies Compete in CVS

7.4.5 Cardiovascular Opportunities and Challenges

7.5 Market Forecast for Gastrointestinal/Metabolic Therapeutic Area, 2016-2027

7.5.1 High Prevalence of Diabetes and GI Conditions

7.5.2 Low Awareness of Diabetes Amongst Population

7.5.3 Drive for Domestic Production of Insulin

7.5.4 EMS’s Generic Esomeprazole an Important Addition

7.5.5 Capturing the Gastrointestinal/Metabolic Disease Opportunity

7.6 Market Forecast for Oncology Therapeutic Area, 2016-2027

7.6.1 Cancer Treatment to Become the Leading Therapeutic Area

7.6.2 Increased Coverage of Cancer Care by Private Health Insurance Providers

7.6.3 What are the Commonest Cancers in Brazil?

7.6.4 Biosimilars Will Help Widen Access to Cancer Drugs

7.6.5 Cristália and Libbs Amongst Leading Oncology Companies

7.6.6 Promising Potential of the Oncology Therapeutic Area

7.7 Market Forecast for Infectious Diseases Therapeutic Area, 2016-2027

7.7.1 Vaccines and Antibiotics Lead Therapeutic Area

7.7.2 Brazil Increasingly Manufacturing its Own Vaccines

7.7.3 First Vaccination Programme Against Dengue Fever

7.7.4 Free Access to HIV Care Despite Concerns About Patent Protection

7.7.5 Chagas Disease and Other Tropical Infections

7.7.6 Long-Term Threat from Zika Virus Epidemic

7.7.7 Importance of Infectious Diseases Compared to Chronic Diseases

7.8 Market Forecast for Other Therapeutic Areas, 2016-2027

8. Domestic Companies in the Brazilian Market

8.1 The Top Ten Domestic Pharmaceutical Companies in 2016

8.2 Multinational Companies Still Own the Majority of the Market

8.3 Domestic Sector Actively Encouraged by Government

8.4 Domestic Firms Control 70% of Generics Market

8.5 EMS: Brazil’s Leading Pharmaceutical Company

8.5.1 Separate Divisions for Different Drug Categories

8.5.2 Full Production and R&D Capability

8.5.3 Legrand and Germed are Key Subsidiaries

8.5.4 Targeted Expansion Overseas

8.6 Hypermarcas: Market Leader in OTC and Branded Generics

8.6.1 Neo Quimica: Ranked Third in the Generics Segment

8.6.2 Subsidiaries Include Mantecorp and Brainfarma

8.7 Medley: Generics Company Owned by Sanofi

8.8 Aché: A Major Acquisition Target in Brazil

8.8.1 Anti-Inflammatory Acheflan Was First Drug Developed in Brazil

8.8.2 Involvement of Aché in Acquisitions Process

8.8.3 Part of Bionovis Collaboration

8.9 Eurofarma: Fourth Largest Domestic Company with Plans to Cover 90% of Latin America

8.9.1 Policy to Make Acquisitions in Latin America

8.10 Teuto Operates Largest Pharmaceutical Complex in Latin America

8.10.1 Melcon Partnership and Other Growth Strategies for Teuto

8.11 Biolab Farmaceutica Leads Cardiology Drugs Market

8.11.1 Partnering with German and Indian Companies

8.11.2 Current Pipeline and Product Launches

8.12 Cristalia: Largest Producer of Anaesthetics in Latin America

8.12.1 Approval from ANVISA to Produce Biosimilar Drugs

8.12.2 Leader in API Manufacturing

8.12.3 Involved in One Third of all PDPs

8.13 Libbs: Key Player in Cancer Treatment

8.13.1 Libbs Secures $106m in Funding from BNDES for New Biotechnology Facility

8.14 União Quimica: Huge Annual Production Capacity

8.14.1 Agreement with Novartis and Possible Public Offering in 2015

8.15 Other Domestic Players Include Laboratório Daudt Oliveira and Hebron

8.16 Biosimilar Collaborations

8.16.1 Bionovis: Conglomerate Developing 8 Biosimilars

8.16.2 Orygen: Conglomerate Aiming to Develop 7 Biologics

8.16.3 Other Biotech Players Include Biomm and Innova

8.16.4 Fiocruz: At the Heart of Multiple PDPs

8.16.5 ANVISA Reform of Brazilian Patent System

9. Multinational Companies in the Brazilian Market

9.1 The Top Ten Multinational Pharmaceutical Companies in Brazil, 2016

9.2 Notable M&A Activity

9.3 Sanofi: Medley Purchase Makes French Giant the Outright Leader

9.3.1 Group Companies Include Sanofi Pasteur and Genzyme

9.3.2 Inventory Mishandling and Dip in 2013 Results

9.4 Novartis: Only Multinational to Produce APIs in Brazil

9.4.1 PDPs and a New $342m Biotechnology Facility in the North East

9.4.2 Pricing and Reimbursement Solutions to Bring Costlier Drugs to Brazil

9.4.3 Investment in Expansion Plans

9.5 Roche: No Regrets About Staying in Brazil

9.5.1 Oncology Opportunity and Herceptin Pricing

9.6 Merck & Co. – Long-Standing Presence in the Brazilian Market

9.6.1 Five Factories and Five Broad Therapeutic Areas

9.6.2 Gardasil Added to SUS in 2013

9.6.3 Joint Venture with Eurofarma and Cristalia

9.7 Pfizer: Pursuing Strategy to Acquire Domestic Manufacturers

9.7.1 Portfolio Ranges from Orphan Biologics to Multivitamins

9.8 Takeda: Expanding its Brazilian Business

9.8.1 Acquisitions of Nycomed and Multilab

9.9 Bayer: Brazil is its Fifth Largest Market

9.9.1 OTC is a Major Focus in Brazil

9.10 AstraZeneca Targets Latin America

9.10.1 Struggling with Loss of Exclusivity and Patent Infringement

9.11 Boehringer Ingelheim: Pain, Cardiovascular and Respiratory Drugs Bolster Strong National Portfolio

9.11.1 Looking to Acquire OTC Brands

9.11.2 Technology Transfer Deal for Parkinson’s Disease

9.12 Merck KGaA Signed PDP with Bionovis for 8 Biosimilars

9.12.1 Two Divisions and Multiple Therapeutic Fields

9.13 Other Notable Multinationals in Brazil

9.13.1 GSK: Vaccines and Technology Transfer Opportunities

9.13.2 Abbott: Humira to Face Biosimilar Challenge in Brazil?

9.13.3 Abbott: Generics and Diagnostics-Led Growth Strategy

9.13.4 Eli Lilly: Investing in Upgrading Pharmaceutical Packaging Facility

9.13.5 Bristol-Myers Squibb: Divesting its Brazilian OTC Portfolio Rights

9.13.6 Baxter Entering Haemophilia Market Via Technology Transfer

9.13.7 Johnson & Johnson: Focusing on Consumer Health and Commodities

9.13.8 BiocadBrazil Farmaceutica

9.13.9 Amgen Signals Brazilian Intent with Bergamo Acquisition

9.13.10 Gilead, Novo Nordisk, Biogen, UCB and Meizler

9.13.11 Other Top Japanese Companies Trail Behind Takeda in Brazil

9.14 Will Multinational Generics Leaders Compete in Brazil?

9.14.1 Teva Targets Brazil

9.14.2 Mylan Acquires Agila to Boost Brazilian Strategy

9.14.3 Actavis May Target Brazil

9.14.4 Ranbaxy and Daiichi Sankyo

9.14.5 Torrent, Glenmark, Strides Arcolab and Biocon Looking to Brazil

9.14.6 Valeant: M&A Drive into the Market

9.15 Brazil as a Pharmaceutical Research Destination

10. Qualitative Analysis of the Brazilian Pharmaceutical Market, 2017

10.1 Strengths, Weaknesses, Opportunities and Threats (SWOT) Analysis

10.1.1 A Crucial Market for the Pharmaceutical Industry

10.1.2 Government Regulation Remains an Issue

10.1.3 One of the Highest Pharmaceutical Tax Rates in the World

10.1.4 Room to Expand in Therapeutic Areas and Geographic Regions

10.1.5 Technology Transfer Uncertainties, IP Protection Doubts and Counterfeiting Issues

10.2 Social, Technological, Economic and Political (STEP) Analysis

10.2.1 Large and Ageing Population Eager to Buy Medicines

10.2.2 Shortcomings of Brazil’s Healthcare System

10.2.3 Government Aims for Greater Self-Sufficiency in Biotechnology and Health IT

10.2.4 Can Economic Growth Keep Pace with Healthcare Costs?

10.2.5 Political Environment Acts as Decisive Influence on the Market

10.2.6 Will BREXIT Affect Free Trade Negotiations with the EU?

11. Conclusions from Our Research and Analysis

11.1 Growth of Brazil’s Pharmaceutical Market Will Outstrip That of More Developed Countries

11.2 Generics Will be the Main Growth Driver

11.3 Technology Transfer Boosts Domestic Production of Originator Drugs

11.4 Generics Market Provides Alternative Option for Multinationals

11.5 Oncology Will be the Main Growth Area in the Brazilian Pharmaceutical Market

11.6 Concluding Comments

Appendices

Some Associated Reports

Visiongain Report Sales Order Form

Appendix A

About Visiongain

Appendix B

Visiongain Report Evaluation Form

List of Tables

Table 2.1 Brazilian Pharmaceutical Market: Revenue ($bn), AGR (%) and CAGR (%), 2016-2027

Table 2.2 Brazilian Pharmaceutical Market by Segment: Revenue ($bn) and Market Share (%), 2016

Table 2.3 Brazilian Pharmaceutical Market by Therapeutic Area: Revenue ($bn) and Market Share (%), 2016

Table 2.4 Brazilian Pharmaceutical Market: Top Ten Companies - Revenue ($bn) and Market Share (%), 2016

Table 3.1 World’ s Largest Pharmaceutical Markets, Revenue ($bn) and Market Share (%), 2016

Table 3.2 Top Latin American Pharmaceutical Markets: Revenue ($bn) and Market Share (%), 2016

Table 3.3 Pharmerging Countries

Table 4.1 Members of FenaSaúde (in Portuguese, with English in brackets), 2017

Table 6.1 Originator Drug, Generic Drug and OTC Drug Segments Forecast: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 6.2 Originator Drug, Generic Drug and OTC Drug Segments: Revenue ($bn) and Market Share (%), 2022

Table 6.3 Originator Drug, Generic Drug and OTC Drug Segments: Revenue ($bn) and Market Share (%), 2027

Table 6.4 Originator Drug, Generic Drug and OTC Drug Segments: Revenue Forecasts ($bn), 2016-2027

Table 6.5 Originator Drug Segment: Revenue Forecasts ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 6.6 Selected Technology Transfer Agreements in Brazil 1985-2013

Table 6.7 Generic Drug Segment: Revenue Forecasts ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 6.8 OTC Drug Segment: Revenue Forecasts ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.1 Brazilian Pharmaceutical Market – Therapeutic Areas: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.2 Brazilian Pharmaceutical Market by Therapeutic Area: Revenue ($bn) and Market Share (%), 2022

Table 7.3 Brazilian Pharmaceutical Market by Therapeutic Area: Revenue ($bn) and Market Share (%), 2027

Table 7.4 CNS Therapeutic Area: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.5 Cardiovascular Therapeutic Area: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.6 Gastrointestinal/Metabolic Therapeutic Area: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.7 Oncology Therapeutic Area: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.8 Infectious Diseases Therapeutic Area: Revenue ($bn, Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 7.9 Other Therapeutic Areas: Revenue ($bn), Market Share (%), AGR (%), CAGR (%), 2016-2027

Table 8.1 Top Ten Domestic Pharmaceutical Companies in Brazil: Revenue ($bn) and Market Share (%), 2016

Table 8.2 EMS Overview

Table 8.3 Hypermarcas Overview

Table 8.4 Medley Overview

Table 8.5 Aché Overview

Table 8.6 Eurofarma Overview

Table 8.7 Teuto Overview

Table 8.8 Biolab Farmacêutica Overview

Table 8.9 Biolab Farmacêutica Pipeline, 2016

Table 8.10 Cristalia Overview

Table 8.11 Libbs Overview

Table 8.12 União Química Overview

Table 9.1 Leading Multinational Companies in the Brazilian Market: Revenues ($bn), Market Shares (%), 2016

Table 9.2 Selected Multinational M&A Activity in the Brazilian Market, 2009-2012

Table 9.3 Sanofi Overview

Table 9.4 Novartis Overview

Table 9.5 Roche Overview

Table 9.6 Merck & Co. Overview

Table 9.7 Pfizer Overview

Table 9.8 Takeda Overview

Table 9.9 Bayer Overview

Table 9.10 AstraZeneca Overview

Table 9.11 Boehringer Ingelheim Overview

Table 9.12 Merck KGaA Overview

Table 10.1 Brazilian Pharmaceutical Market: SWOT Analysis 2017

Table 10.2 Brazilian Pharmaceutical Market: Opportunities and Threats, 2016

Table 10.3 Brazilian Pharmaceutical Market: STEP Analysis, 2017

List of Figures

Figure 1.1 Product Segments of Brazilian Pharmaceutical Market

Figure 1.2 Main Therapeutic Areas Within Brazilian Pharmaceutical Market

Figure 2.1 Brazilian Pharmaceutical Market: Revenue ($bn) 2016-2027

Figure 2.2 Brazilian Pharmaceutical Market by Segment: Market Share (%), 2016

Figure 2.3 Brazilian Pharmaceutical Market by Therapeutic Area: Market Share (%), 2016

Figure 2.4 Brazilian Pharmaceutical Market: Top Ten Companies – Market Share (%), 2016

Figure 3.1 Top Ten Global Economies, 2017

Figure 3.2 Top Ten Global Economies, 2030

Figure 3.3 World’s Largest Pharmaceutical Markets by Market Share (%), 2016

Figure 3.4 Top Latin American Pharmaceutical Markets: Market Share (%), 2016

Figure 3.5 BRIC Countries Pharmaceutical Market Revenue ($bn), 2016

Figure 4.1 Public Healthcare Versus Private Healthcare: Market Share (%), 2017

Figure 5.1 Doctors per 1,000 Inhabitants by Brazilian Region, 2013

Figure 5.2 Brazil: Regional Population Shares (%), 2013

Figure 5.3 Brazilian Pharmaceutical Market Shares (%) by Region, 2012

Figure 5.4 Brazilian GDP Shares (%) by Region, 2013

Figure 6.1 Originator Drug, Generic Drug and OTC Drug Segments: Market Share (%), 2022

Figure 6.2 Originator Drug, Generic Drug and OTC Drug Segments: Market Share (%), 2027

Figure 6.3 Originator Drug, Generic Drug and OTC Drug Segments: Revenue Forecasts ($bn), 2016-2027

Figure 6.4 Originator Drug, Generic Drug and OTC Drug Segments: Revenue ($bn), 2016,2022, 2027

Figure 6.5 Originator Drug Segment: Revenue ($bn) and AGR (%), 2016-2027

Figure 6.6 Drivers and Restraints for Patented Pharmaceuticals, 2017

Figure 6.7 Generic Drug Segment: Revenue ($bn) and AGR (%), 2016-2027

Figure 6.8 Drivers and Restraints for Generic Drugs, 2017

Figure 6.9 Brazilian Biologics Market Breakdown: Revenue ($bn) and Market Share (%), 2016

Figure 6.10 Brazilian Biologics Market Breakdown: Revenue ($bn), 2016, 2021 and 2027

Figure 6.11 OTC Drug Segment: Revenue ($bn) and AGR (%) 2016-2027

Figure 6.12 Drivers and Restraints for OTC Drugs, 2017

Figure 7.1 Brazilian Pharmaceutical Market by Therapeutic Area: Market Share (%), 2022

Figure 7.2 Brazilian Pharmaceutical Market by Therapeutic Area: Market Share (%), 2027

Figure 7.3 Brazilian Pharmaceutical Market by Therapeutic Area: Revenue Forecasts ($bn), 2016-2027

Figure 7.4 Brazilian Pharmaceutical Market by Therapeutic Area: Revenue ($bn), 2016, 2022, 2027

Figure 7.5 CNS Therapeutic Area: Revenue ($bn) and AGR (%), 2016-2027

Figure 7.6 Drivers and Restraints for CNS Conditions, 2017

Figure 7.7 Cardiovascular Therapeutic Area: Revenue ($bn) and AGR (%), 2016-2027

Figure 7.8 Drivers and Restraints for the Cardiovascular Therapy Area, 2017

Figure 7.9 Gastrointestinal/Metabolic Therapeutic Area: Revenue ($bn) and AGR (%), 2016-2027

Figure 7.10 Drivers and Restraints for Gastrointestinal/Metabolic Therapy Area, 2017

Figure 7.11 Oncology Therapeutic Area: Revenue ($bn) and AGR (%), 2016-2027

Figure 7.12 Estimated Cancer Incidence for Males in Brazil, 2016

Figure 7.13 Estimated Cancer Incidence for Females in Brazil, 2016

Figure 7.14 Drivers and Restraints for the Oncology Therapeutic Area, 2017

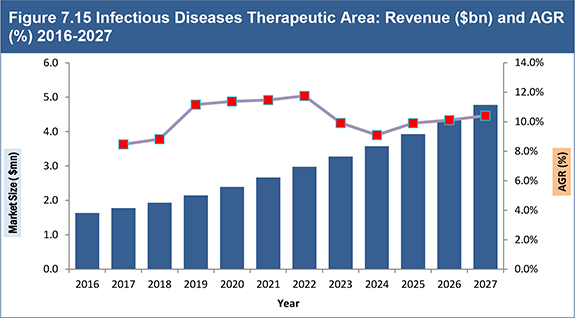

Figure 7.15 Infectious Diseases Therapeutic Area: Revenue ($bn) and AGR (%) 2016-2027

Figure 7.16 Drivers and Restraints for the Infectious Disease Therapeutic Area 2017

Figure 7.17 Other Therapeutic Areas: Revenue ($bn) and AGR (%), 2016-2027

Figure 8.1 Top Ten Domestic Pharmaceutical Companies in Brazil: Market Share (%), 2016

Figure 8.2 Aché Product Portfolio Breakdown (%), 2013

Figure 9.1 Leading Multinational Companies in the Brazilian Market: Market Shares (%), 2016

Figure 11.1 Brazilian Pharmaceutical Market: Overall Revenue ($bn) and AGR (%), 2016-2021

Figure 11.2 Brazilian Pharmaceutical Market: Overall Revenue ($bn) and AGR (%), 2021-2027

Figure 11.3 Brazilian Pharmaceutical Market by Segment: Revenue ($bn), 2016-2021

Figure 11.4 Brazilian Pharmaceutical Market by Segment: Revenue ($bn), 2021-2027

Figure 11.5 Top Ten Companies in the Brazilian Pharmaceutical Market: Revenue ($bn), 2016

Figure 11.6 Brazilian Pharmaceutical Market Therapeutic Area Breakdown: Revenue ($bn), 2016-2021

Figure 11.7 Brazilian Pharmaceutical Market Therapeutic Area Breakdown: Revenue ($bn), 2021-2027